Sentiment analysis (stock exchange)

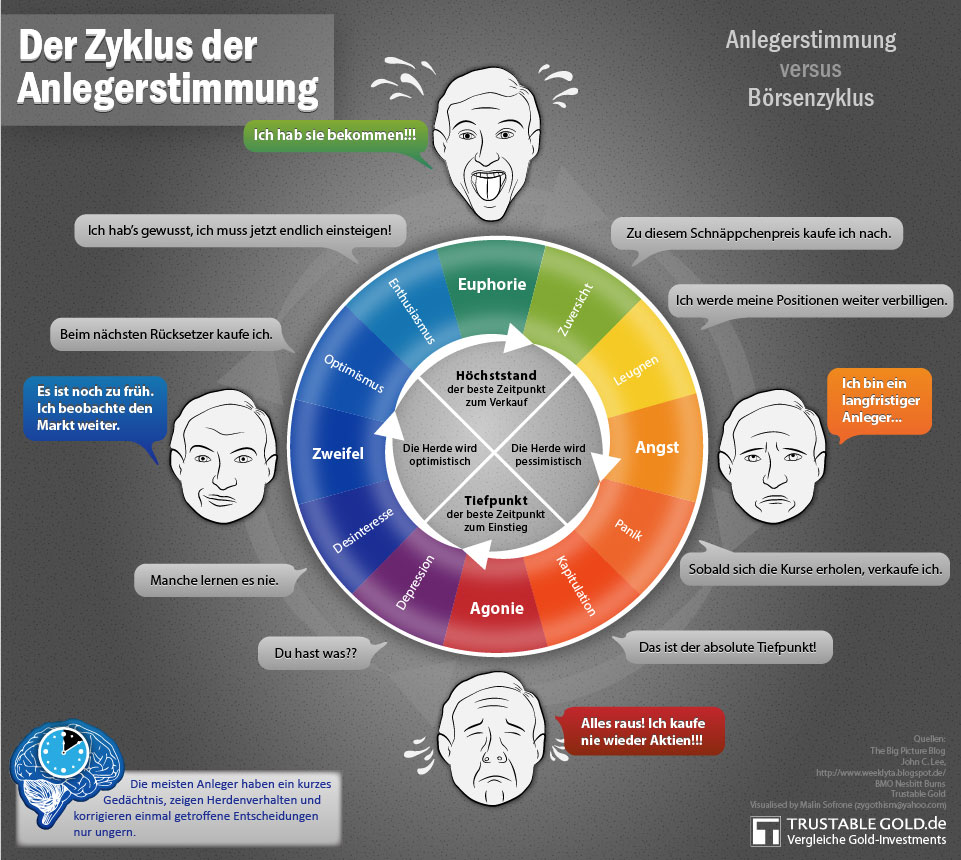

By means of sentiment analysis (“sentiment” for sensation, feeling ) one tries in the context of financial analysis to interpret the moods of investors on the stock market in terms of their significance for the development of securities prices. The sentiment analysis goes beyond chart analysis in that it not only looks at the price development itself, but also in terms of behavioral financeaims directly at exploring investor psychology in a given market situation. In the opinion of the sentiment analysts, investor sentiments can provide additional help in developing well-founded assumptions about future price developments, which then form the basis of investment or short-term trading decisions.

Under sentiment refers to a market the sum of the moods of the individual players, so the general market sentiment.

Indicators

Possible indicators for the sentiment are:

- Explicit surveys among investors (e.g. survey by the American Association of Individual Investors ( AAII ), sentix survey),

- the put-call ratio , i.e. the ratio of traded puts to calls on an options exchange. This shows how many investors are betting on falling (puts) or rising prices (calls).

- Optimistic or pessimistic attitude of the stock market letter authors,

- general media reports (the frequency of reporting is also interesting) with recommendations or opinion-gathering on stocks, foreign exchange, etc. Ä.,

- current cash inflows, cash holdings in funds,

- Insider trades,

- the mark-up or mark-down of the price of a closed-end investment fund to its net asset value ,

- the number of initial public offerings (IPOs) and the subscription yields.

example

If the extent of the determined optimism (" bullish sentiment") or pessimism ("bearish sentiment") goes beyond a certain empirically known normal measure, this can serve as a " contra-indicator ". That is, it is assumed that such stronger sentiment swings herald price turning points. There are two basic assumptions behind this:

- If the great majority of investors have already invested, there are just a few left who could buy more and thus drive prices up; Conversely, of course, the same applies: If the majority of investors have not invested, only a few can sell and thus depress prices.

- If investors have invested, they will be optimistic about the expected further course of the price, if they have not invested, they will be pessimistic. To be pessimistic about the future performance of securities, but to have invested at the same time, would of course not make much sense under normal circumstances.

To determine the prevailing mood in a market situation, direct methods are used (such as surveys in a panel of investors) and various indirect methods . The latter include, for example, the put-call ratio or the consideration of the relationship between the purchases of “in-the-money” discount certificates and “out-of-the-money” papers.

In addition to the sentiment analyzes directly related to stock exchange trading, there are other sentiment surveys that are relevant to the economy as a whole, such as the sentiment section of the IFO business climate index and the “ ZEW ”.

Problems

The interested user of sentiment data is now offered an almost unmistakable abundance of the most varied of indicators, which in one way or another should be suitable for quantitatively depicting “investor sentiment”. Very often the first impression is that the results are diametrically opposed. There are several reasons for this. The sentiment data collected through direct surveys in the stock exchange sector suffer in most cases from the fact that the type of survey, particularly the selection of the sample (panel), in no way meets the basic quality requirements ( randomization , sample size, etc.) common in the social sciences . Often it is not even clear to which population (amount of data / objects / people to be represented by a sample) the samples are to be assigned to. Since investor behavior and thus also the sentiment of short, medium and long-term, institutional and private investors often differ significantly, one could certainly assume different populations here.

It also happens that investors are in principle positive for the market and are correspondingly bullish, but that they are only in the market with small amounts ("optioning") and wait with larger commitments until certain technical resistance has been overcome in the long term .

Since the development of the gold price, bond market (e.g. the Bund future ), volatility, market turnover or the price developments of so-called “safe-haven” currencies such as US dollars or Swiss francs are often used as indirect indicators for market sentiment, the picture remains often very diffuse. The professional user of stock market data therefore has no choice but to work out an overall impression from the various pieces of the mosaic for his specific purpose, taking into account that precisely the most important, long-term market participants do not let themselves "look into the cards".

See also

literature

- Joachim Goldberg, Rüdiger von Nitzsch: Behavioral Finance . Verlag FinanzBook, Munich 1999, ISBN 978-3-89879-100-7 .

Web links

{kind=link}

Individual evidence

- ↑ Duden - Sentiment, das. In: duden.de. Retrieved April 13, 2016 .

- ↑ Nadja Siebenmann: The psyche of private investors. In: Basler Zeitung. November 29, 2010, accessed November 30, 2010 .