Insurance certification

An insurance securitization (English insurance linked security , hence the abbreviation ILS) is a bond , by the securitization is characterized by insurance risks. The creditor's claim consists of payment claims against a special purpose vehicle that uses its funds exclusively to acquire insurance risks through reinsurance contracts and securitizes these as securities. The sellers of receivables in such a transaction are usually insurance companies who make parts of their insurance risks tradable in order to refinance themselves .

To this asset class include catastrophe bonds , life insurance bonds (English life bonds ) and collateralized debt obligations .

General

With insurance securitization, the insurance industry has had a new instrument for risk transfer and refinancing since the early 1990s . The volumes grew steadily in the years up to the worsening of the financial market crisis in 2008. Risks from catastrophes and changes in mortality as well as burdens from newly developed business areas were transferred to the capital markets. Future premium flows have been pre-financed through securitisations and enable insurance companies to allocate capital more efficiently.

Significance for the insurance industry

The insurance industry has a wide range of business types used to cover risks. Some types of risk, such as counterparty risk, credit risk and mortgage risk, are also assumed in one form or another by banks. Other types of risk, such as mortality, longevity and disaster, are insurance-specific and rather unknown outside of the insurance sector.

The traditional methods of reinsurance and retrocession are available to insurers for risk transfer . As an additional option, the alternative risk transfer with various instruments has been developed in recent decades . An alternative is the risk transfer to the capital market - in contrast to the risk transfer within the insurance sector, which is described as traditional. Insurance securitisations are a sub-area of alternative risk transfer.

Types of insurance certification

In property insurance

Catastrophe bonds are the best known form of securitization in property insurance . They cover natural disasters such as storm and earthquake risks as well as major man-made losses. The latest innovations are also securitizations for car insurance and covers for credit risk portfolios.

In life insurance

Life insurance securitisations are used to cover reservation requirements, to pre-finance income and to transfer risk. The securitization of the purchase of life insurance contracts on the secondary market ( life settlement ) is another form of life insurance securitization .

Collateralized Debt Obligations

Insurance-linked collateralized debt obligations are a special form of securitization. In addition to subordinated bonds from insurance companies, reinsurance claims and risks from catastrophe bonds were bundled and securitized.

The stakeholders in the securitization process

Sponsors

Insurance companies (direct insurers or reinsurers) appear on the market as sponsors (also called initiators) of insurance securitisations. The main motives for choosing insurance securitization are primarily the transfer of risk, as well as capital savings or the development of new groups of investors.

Rating agencies, risk modelers and bond insurers

Rating agencies , risk modelers and bond insurers have an interest in standardizing the market for insurance securitisations. Rating agencies assess the likelihood that the promised interest and principal payments will be made properly. Risk modelers assess the probability of occurrence of damage and its amount. Bond insurers provide additional collateral in the form of insurance for interest payments and repayment of the securities.

Investors

Insurance securitisations give investors an option to improve risk diversification within bonds as an asset class, as the typical insurance risks are poorly correlated with other bond risks. In the context of portfolio management , this can improve the risk / reward ratio; the default risks are spread through better diversification.

The design of triggers (payment trigger mechanisms in the event of damage) has an impact on the return on the securitized bonds. With the rapid growth of the catastrophe bond market, investment funds (UCITS) that are approved for public distribution in certain EU countries have successfully established themselves. Companies such as LGT, Twelve Capital, GAM, Schroders, Plenum Investments, Entropics should be mentioned.

Arrangers

As arrangers of insurance securitisations, in addition to banks in their role as capital collection agencies, insurance companies can also act. In addition, placement capacities were built up with large insurance brokers .

Auditors and regulators

The systems in Europe and the US are very different in terms of accounting and insurance supervision .

Lawyers

Lawyers are involved in drawing up the contractual documentation. You are in contact with almost all interest groups and therefore have a very good overview of the securitization process.

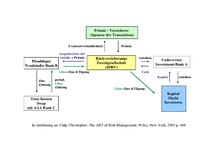

Simplified scheme of an insurance securitization

- Phase 1: The primary insurer (sponsor) decides to transfer the risk by means of insurance securitization and establishes a special purpose vehicle .

- Phase 2: The sponsor transfers the portfolio by concluding a reinsurance contract with the special purpose vehicle

- Phase 3: The special purpose vehicle instructs a bank to issue bonds.

- Phase 4: The bonds are placed with capital market investors and the proceeds from the issue are paid into a deposit that is managed by a trustee . The trustee can use the cash to buy securities for higher returns.

- Phase 5: Interest and redemption payments on the portfolio are guaranteed to investors by a bank; the bank hedges itself for this purpose, typically by means of a total return swap.

- Phase 6a: If no event occurs through which the bond becomes due (trigger event), the capital is repaid to the capital market investors when it finally matures.

- Phase 6b: If a trigger event occurs, the investors lose part or all of the assets brought in, depending on the contractual agreement.

Effects of the financial market crisis

The collapse of the investment bank Lehman Brothers and the subsequent financial market crisis revealed weaknesses in insurance securitisations that the players in the financial markets had not expected. Lehman Brothers was involved in the insurance securitization market as arranger, underwriter, total return swap partner and investor. Problem areas are:

- Phases 1 and 2: If sponsors (like the AIG back then) get into trouble, the holdings are managed like the sponsor's other businesses. The supervisory authorities have a duty to protect the interests of policyholders.

- Phase 3: The banks were badly affected by the financial crisis and at times were barely in a position to provide underwriting. The market for property insurance securitisations was disrupted in the second half of 2008, with very few new issues being placed, but secondary market trading continued and with few losses in value. As early as 2009, not only renewal transactions but also new business were placed on the market. The market has been returning to normal since 2010.

- Phase 4: The willingness of investors to buy ILS, especially against the background that the returns for investments in corporate bonds with comparable credit ratings temporarily generate higher returns did not decrease significantly, as ILS have only very little correlation with other asset classes.

- Phase 5: If the bank that has committed itself to compensate for losses in the total return swap gets into difficulties, the business basis for the entire securitization is in jeopardy. Banks in this role are required to have a very good credit rating.

- Phase 6: The swap rates were very volatile during the crisis and rose sharply at times. As a result, the interest rate promises made by ILS, which are mostly based on such swap rates, have increased. As a result, less volatile rates for short-term government bonds were set as the basis for some transactions.

The rating agencies have also come under great pressure due to their misjudgments of the creditworthiness of mortgage securitizations . A strong separation of the risk assessment from the mandate and stricter standards should regain the trust of investors.

Market for ILS

Due to the very low correlation with other products, the prices for ILS have remained stable even during the financial market crisis. Although the Fukushima nuclear disaster led to the default of three bonds, it barely affected the growth in issue volumes and the market values of the other ILS.

Securitisations to cover US life insurance reserve requirements have become increasingly unattractive with the elimination of the monoliners. Most monoline insurance companies came under great pressure or failed completely during the financial market crisis. There is currently no longer any cover available for long-term life insurance ILS. This made the structures unattractive for investors due to their complexity. To hedge against longevity risks, secured swap structures with banks currently appear more attractive than securitisations. Mortality risks are still hedged to a small extent via ILS.

In addition, as a regulated company, insurance companies must meet minimum capital requirements. It was expected in advance that ILS techniques would become more important with the introduction of the new Solvency II supervisory regime in Europe in 2012.

literature

As sources:

- Christopher L. Culp: The ART of Risk Management: Alternative Risk Transfer, Capital Structure, and the Convergence of Insurance and Capital Markets . Wiley, New York 2002, ISBN 978-0-471-12495-5 (English).

- Structure and the Convergence of Insurance and Capital Markets . Wiley, New York 2002, ISBN 0-471-12495-8 (English).

- Christoph Weber: Insurance Linked Securities - The Role of the Banks . Gabler, Wiesbaden 2011, ISBN 978-3-8349-2860-3 (English).

Further literature:

- Erik Banks: Alternative Risk Transfer: Integrated Risk Management through insurance, reinsurance, and the capital markets . Wiley, Chichester 2004, ISBN 0-470-85745-5 (English).

- Peter Liebwein: Classic and Modern Forms of Reinsurance . VVW, Karlsruhe 2000, ISBN 3-88487-794-1 .

- Mischa Ritter: Securing Disaster Risk Using Capital Markets: A Critical Assessment . Gabler, Wiesbaden 2006, ISBN 3-8350-0334-8 .

Web links

Individual evidence

- ^ Christoph Weber: Insurance Linked Securities - The Role of the Banks . Gabler, Wiesbaden 2011, ISBN 978-3-8349-2860-3 , pp. 2 (English).

- ^ Christopher L. Culp: The ART of Risk Management: Alternative Risk Transfer, Capital Structure and the Convergence of Insurance and Capital Markets . Wiley, New York 2002, ISBN 0-471-12495-8 , pp. 333-334 (English).

- ^ Peter Albrecht, Heinrich R. Schradin: Alternative risk transfer: securitization of insurance risks . University of Mannheim, Mannheim 1998, p. 2 .

- ↑ Ernst N. Csiszar: An Update on the Use of Modern Financial Instruments in the Insurance Sector . In: The Geneva Papers . tape 32 , 2007, p. 319-331 .

- ↑ Link text ( Memento of the original from January 21, 2012 in the Internet Archive ) Info: The archive link was inserted automatically and has not yet been checked. Please check the original and archive link according to the instructions and then remove this notice. (PDF file; 992 kB) Securitization of Life Insurance Assets and Liabilities, J. David Cummins, The Wharton School, Bryn Mawr, January 3, 2004

- ↑ Link text How CDOs can make excess capital productive, Laurent Dignat, New York, 2008

- ^ Christopher L. Culp: The ART of Risk Management: Alternative Risk Transfer, Capital Structure and the Convergence of Insurance and Capital Markets . Wiley, New York 2002, ISBN 0-471-12495-8 , pp. 470-471 .

- ^ Christoph Weber: Insurance Linked Securities - The Role of the Banks . Gabler, Wiesbaden 2011, ISBN 978-3-8349-2860-3 , pp. 268-271 .

- ↑ Link text (PDF file; 1.14 MB) Insurance Linked Securities, First Quarter Update 2011, AON Benfield, Chicago, 2011

- ↑ a b Market for catastrophe bonds is booming, Börsenzeitung, Frankfurt, January 13, 2011, p. 5.

- ^ A b Christoph Weber: Insurance Linked Securities - The Role of the Banks . Gabler, Wiesbaden 2011, ISBN 978-3-8349-2860-3 , pp. 272-276 .