Three pillar system (Switzerland)

The three-pillar system in Switzerland is the old-age, disability and survivors' insurance based on three pillars - with different financing as the main pillars of the provision. This article on the three-pillar system presents all elements (compulsory and voluntary) of social and private provision and their interaction. This was stipulated in the Federal Constitution (BV) in 1972 after a vote; the template bears the signature of the then Federal Councilor Hans-Peter Tschudi . It finally came into force on January 1, 1985. In the 1972 vote, it was contrasted with a popular initiative launched by the Labor Party in 1969 , which provided for a uniform pension fund system, but only 15.6% of the electorate approved this move.

The representation of the three-pillar principle is different in practice; in particular, opinions regarding the insurance companies to be mentioned under the second pillar may diverge. In the Federal Constitution Art. 111, when the expression "... three pillars ..." is used for the second pillar, only occupational benefits in the narrower sense of occupational benefits, namely occupational benefits under the BVG (law on occupational benefits). In many cases, however, when a comprehensive three-pillar system is presented in the second pillar, all insurances in connection with employment are mentioned.

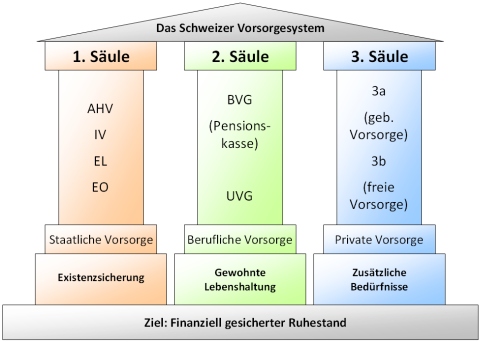

- First pillar: with the exception of supplementary benefits, compulsory pay-as-you-go insurance for the whole population, to secure livelihoods and avoid poverty:

- Old-age and survivors' insurance (AHV)

- Disability Insurance (IV)

- Supplementary benefits (EL) for AHV and IV

- Benefits in accordance with the Income Compensation Ordinance (EO) for military service, civil defense service, community service or maternity

- Benefits from the unemployment insurance (ALV)

- Second pillar: funded insurance for the working population to cover the usual cost of living , consisting of:

- Compulsory occupational pension benefits (commonly referred to as the pension fund)

- Benefits from the extra-mandatory occupational pension scheme (integration of voluntary additional benefits in the occupational pension scheme)

- Compulsory accident insurance benefits

- Benefits from the additional insurance voluntarily organized by the employer in addition to the compulsory accident insurance

- Benefits from the daily sickness allowance insurance voluntarily organized by the employer

- Third pillar: voluntary, individual, tax-privileged private self-provision in addition to the first and second pillar:

- Tied pension provision (3a)

- Free provision (3b)

The first pillar

The first pillar covers the livelihood of the entire population in the following areas:

- Old-age provision: Old-age and survivors' insurance (AHV)

- Death of the spouse or the spouse or one of the parents; in particular survivors 'benefits: old-age and survivors' insurance (AHV). If it is a registered partnership , the surviving part also receives a pension. It currently corresponds to the widower's pension.

- Loss of wages due to disability: disability insurance (IV)

With the exception of the supplementary benefits, the first pillar is financed according to the pay-as-you-go system : the contributions received are used immediately to finance the pensions . The contributions are divided between the employee and the employer and amount to 5.275% each

Just like the 1st pillar, it is mandatory to take out health insurance in Switzerland , since the entire population must be insured for treatment costs resulting from an accident or illness. As an exception, the employer, i.e. the company, is responsible for working people in the event of an accident, whereas in the case of non-working people, the medical costs in the event of an accident are covered by the mandatory accident insurance. are covered by health insurance.

Income compensation scheme

The income compensation scheme partially covers loss of wages due to military, community service or civil defense operations. Since July 1, 2005 , maternity benefits have also been available from the income compensation scheme for mothers who interrupt or give up their employment because of motherhood.

The second pillar

In a broader sense, the whole of the second pillar can be referred to as “occupational pension provision”, as all working people are insured here. In a narrower sense, however, “occupational benefits” is understood to mean occupational benefits under the BVG (law on occupational benefits) as a sub-area of the second pillar (see under BVG).

The benefits of the second pillar supplement the benefits of the AHV / IV in old age, in the event of disability and in the event of the death of the provider. The aim of the second pillar is to supplement the first pillar to secure the cost of living.

Occupational benefits according to the law on occupational benefits (BVG)

The occupational pension scheme according to the BVG refers to that part of the second pillar that complements the first pillar in the areas of old-age provision and the consequences of illness-related disability and death. It is offered by pension funds , insurance companies and autonomous collective foundations. In everyday language, the “occupational pension plan” is therefore also called the pension fund. When it comes to occupational pensions, there is sometimes competition . The employer can choose from various providers. Larger companies and the administration usually have their own pension fund. Every employee of a company with a total annual income of more than CHF 21,330 is compulsorily insured in the employer's pension fund. Self-employed persons and employees who are not subject to mandatory insurance can take out voluntary insurance.

The assessment basis is the coordinated annual salary, which means the AHV salary minus the coordination deduction of CHF 24,885 (as of 2020). From this coordinated annual salary, the retirement credit is calculated as a percentage of the insured salary according to age. The following applies to the savings scale:

| Age | Retirement credit in% of the insured salary |

|---|---|

| 25 to 34 | 7.0% |

| 35 to 44 | 10.0% |

| 45 to 54 | 15.0% |

| 55 to 64/65 | 18.0% |

Accident insurance

Compulsory accident insurance bears the main burden of the consequences in the event of an accident (loss of wages in the short and long term, treatment costs, survivors' benefits). It is supplemented by benefits from the first pillar (disability insurance).

Many industries (including the construction industry) have to take out accident insurance from the semi-public Swiss accident insurance company SUVA . In other industries, employers can choose between different insurance companies . There are no service differences between the various providers, as the services are defined by law. The premiums were regulated by industry until the end of 2006 (community statistics, based on the recommendation of the insurance association with state blessing), the premium scope was only within the framework of the administrative cost rate included in the premium, which was regularly reduced by several percentage points for large contracts. Since 2007 the insurance association has not been allowed to make recommendations and every insurance company is free to use its own statistics and apply its own tariffs.

Non-working people and children must be insured with the health insurance company for treatment costs as a result of an accident .

Daily sickness benefit insurance

In the event of illness-related incapacity for work, the daily sickness allowance insurance to be taken out voluntarily by the employer pays the wage replacement, usually for two years, until benefits from the disability insurance (first pillar) and the pension fund (the "occupational pension", second pillar) begin.

Freedom of movement

In accordance with the Federal Act on Compulsory Occupational Retirement, Survivors' and Disability Pension Plans (BVG), an insured person is entitled to the entire termination or vested benefits upon leaving the BVG compulsory system. An exit can u. a. be justified by the following situations: emigration, training or further education, self-employment, maternity leave, unemployment or divorce. In certain cases, the vested benefits can be paid out in cash. These include emigration to a non-EU country or minor (if the termination benefit is less than the annual contribution of the insured person). If no payment is possible or desired, the vested benefits will be transferred to a vested benefits account of a vested benefits institution .

The third pillar

The third pillar is self-provision; It is intended to reduce or close pension gaps from the first and second pillars. Such gaps exist in particular in the accumulation of retirement capital to finance the third phase of life and in the case of disability and survivors' benefits in the event of illness.

The third pillar is voluntary and, together with the first and second pillars, serves to maintain the usual standard of living in the event of incapacity for work or retirement. There are banking solutions and insurance solutions; private bank savings accounts are also included in the third pillar. With both solutions, money is saved for old-age provision (funded procedure). In contrast to the insurance solution, the risk of disability and death is not covered with the banking solution. In the third pillar, a distinction is made between two types of provision: the tied (pillar 3a) and free provision (pillar 3b).

Pillar 3a: restricted pension

The fixed pension plan (Pillar 3a) is a form of provision, based on the constitutional three-pillar principle. Pillar 3a is funded by the federal government so that contributions to pillar 3a are tax-deductible. The legal details are regulated in the Ordinance on Tax Deduction for Contributions to Recognized Pension Plans (BVV3). The capital saved in pillar 3a is intended to finance old age and is therefore earmarked. However, the legislature provides for exceptions in order to withdraw the money early for defined purposes.

Approved forms of provision

The BVV 3 statutory ordinance only permits two types of provision:

- Bound pension agreement with a bank foundation (the money is managed by the associated bank).

- Tied pension insurance with a Swiss insurance company.

Bound pension agreement

Banks now offer three options within Pillar 3a .

- Retirement account

- The most common form of provision is the provision account. The interest rate is higher than that of a normal savings account . The higher the interest, the higher the total capital in old age (see compound interest effect ).

- Securities solution (pension fund)

- The pension money is invested in securities ( shares , money collection points for investors (funds) and bonds ). The maximum permissible security quota of the individual pension funds is regulated by law in the Ordinance on Occupational Old-Age, Survivors' and Disability Pension Plans (BVV 2). Under certain circumstances, securities solutions can achieve better returns, but with a higher risk of loss.

- Structured, capital-protected pension products

- Banks also offer structured pension solutions with capital protection (see structured financial product ). The bank invests the money in defined financial products. At the end of the total term, the customer will be credited with the invested capital together with the interest earned on his pension account.

Tied pension insurance

Swiss insurance companies can also offer pillar 3a pension products. The products differ in one essential point from the offerings of the banks. The insurance product has always integrated insurance protection.

- Pension policy 3a

- The pension policy 3a combines risk protection (disability and death) with a guaranteed retirement capital. In addition, a premium exemption can be insured in the event that disability occurs during the contract period.

- Unit-linked pension policy fund 3a

- The unit-linked pension policy 3a combines risk protection (disability and death) with a securities saving process. In addition, a premium exemption can be insured in the event that disability occurs during the term of the contract. The maximum permissible security quota for the individual pension policies is regulated by law in the Ordinance on Occupational Old-Age, Survivors' and Disability Pension Plans (BVV 2). Under certain circumstances, unit-linked pension policies can achieve better returns, but at the same time with a higher risk of loss.

Legal requirements and limitations

Basically, anyone can use the column 3a, the subject IV in Switzerland AHV / employment is. It is also open to people who receive daily unemployment benefits.

- Annual maximum amounts

The maximum amounts that can be paid in each year are determined by their tax deductibility. The maximum annual contribution depends on whether the taxable person belongs to an occupational pension fund ( pension fund ) or not.

| year | Compulsory AHV / IV and affiliated to a pension fund | Compulsory AHV / IV without a pension fund |

|---|---|---|

| 2019 | CHF 6,826 | 20% of the net earned income, maximum: CHF 34,128 |

| 2018 | CHF 6'768 | 20% of the net earned income, maximum: CHF 33,840 |

| 2017 | CHF 6'768 | 20% of the net earned income, maximum: CHF 33,840 |

| 2016 | CHF 6'768 | 20% of the net earned income, maximum: CHF 33,840 |

| 2015 | CHF 6'768 | 20% of the net earned income, maximum: CHF 33,840 |

| 2014 | CHF 6'739 | 20% of the net earned income, maximum: CHF 33,696 |

| 2013 | CHF 6'739 | 20% of the net earned income, maximum: CHF 33,696 |

| 2012 | CHF 6,682 | 20% of the net earned income, maximum: CHF 33,408 |

| 2011 | CHF 6,682 | 20% of the net earned income, maximum: CHF 33,408 |

| 2010 | CHF 6'566 | 20% of net earned income, maximum: CHF 32,832 |

| 2009 | CHF 6'566 | 20% of net earned income, maximum: CHF 32,832 |

| 2008 | CHF 6,365 | 20% of net earned income, maximum: CHF 31,842 |

| 2007 | CHF 6,365 | 20% of net earned income, maximum: CHF 31,842 |

| 2006 | CHF 6'192 | 20% of the net earned income, maximum: CHF 30,960 |

| 2005 | CHF 6'192 | 20% of the net earned income, maximum: CHF 30,960 |

| 2004 | CHF 6'077 | 20% of the net earned income, maximum: CHF 30,384 |

| 2003 | CHF 6'077 | 20% of the net earned income, maximum: CHF 30,384 |

- Tax deductibility of the pension funds saved

Payments into the third pillar can be deducted from the taxable income within the framework of the statutory maximum contributions and thus directly reduce the taxable income. In addition, capital increases (interest on the pension account or the increase in value in securities solutions or insurance policies) are tax-free.

Withdrawal of pension funds

Due to the tax privileges, there are legally limited purchase options. A distinction is made between early and regular withdrawal. If the account holder dies before regular retirement, a legally regulated order of payments comes into effect.

Early withdrawal

Early withdrawal means that the capital is withdrawn before actual retirement. The following exceptions justify an early withdrawal of pillar 3a:

- Financing owner-occupied homes or repaying existing mortgages

- Buying into a pension fund

- Taking up self-employment or changing previous self-employment

- Leaving Switzerland ( emigration )

- A disability pension is drawn and the risk of disability is not covered by additional insurance

Death of the pension fund member before regular retirement

If the owner of the restricted pillar 3a dies, the capital must be paid out in accordance with a statutory regulation. The BVV 3 ordinance is decisive for this.

- The surviving spouse or registered partner has absolute priority

- Without a spouse or registered partner, the benefit is transferred to:

- The direct descendants or

- Natural persons for whose maintenance the deceased was responsible or

- People who have been living in a relationship with this company without interruption in the past five years until their death or

- People who have to support one or more children together

- parents

- siblings

- Other heirs as in Testament mentions

Ordinary pay (retirement)

The tied pension funds may be paid out no earlier than five years before reaching the normal AHV retirement age. However, they are due at the latest when you reach AHV retirement age (64 or 65 years). People who continue their employment can withdraw from pillar 3a until they cease employment for a maximum of 5 years up to 69 or Postpone 70 years.

Tax treatment when withdrawing pension funds

Lump-sum payments from pillar 3a (regardless of whether they are withdrawn early or in the normal way) are taxed separately. At the federal level , they are subject to a full annual tax, which is calculated at a fifth of the tariffs of the ordinary federal tax . Cantons and communes apply different tax rates. However, they are treated separately from other income with a reduced tax rate. The paid-out capital is transferred to private assets. The income from the credit is therefore subject to withholding tax and must be declared on the tax return.

Pillar 3b: unrestricted provision

Pillar 3b includes types of pension that are not tied to a contract with a specific term, i.e. H. which the policyholder can have paid out or canceled practically at any time. Above all, this includes bank savings accounts. The contributions to pillar 3b are not tax-privileged.

Fund policies, on the other hand, are tax-privileged after 10 years and have a specific term. However, early withdrawals are possible.

See also

literature

- Ingrid Katharina Geiger: Basics of social insurance in Switzerland . Compendio Bildungsmedien AG, Zurich 2010, ISBN 978-3-7155-9379-1 ( online )

Web links

- Federal Social Insurance Office

- Federal law on old-age, survivors' and disability insurance

- Old age , administration of old-age and survivors' insurance (AHV) and pension funds in the history of social security in Switzerland

- Page no longer available , search in web archives: Advice Federal Social Insurance Office

- Information about the three pillar concept of Swiss pension provision

- Graphics as of 2009 (finanzmonitor.com) accessed on December 30, 2012

- Page no longer available , search in web archives: Information from the Swiss legislature on pillar 3a

- Contribution in Kassensturz on the topic of saving in Pillar 3a

{kind=link}

Individual evidence

- ↑ http://www.kommunisten.ch/index.php?article_id=928 , accessed on April 7, 2020

- ↑ Leaflet 2020 (valid from January 1, 2020).

- ↑ Page no longer available , search in web archives: Regulations for emigration to the European Union .

- ↑ "Swiss Federal Constitution Article 111 Three Pillar Principle" .

- ↑ "BVV3 - Regulation on the tax deductibility of Contributions to Recognized Pension Plans" .

- ↑ a b "Articles 49-59 BVV2 - Ordinance on occupational old-age, survivors' and disability benefits" .