Municipal finance

Under municipal finances (or municipal finance ) refers to all financial activities of local authorities ( cities , municipalities and associations of municipalities ) including their communal enterprise / public companies , as reflected in the budget ( Kameralistik ) or annual financial statements ( Doppik reflect).

General

The term municipal finances thus includes the income and expenditure or income and expenses as well as the assets and debts of the municipalities. Sometimes the term is narrowed down to the income side of the household. The municipal finances form part of the state finances in the broader sense.

Municipal financial activities

Depending on whether the accounting system is based on the double- entry method or based on cameralistics, a distinction must be made between income / receipts, expenses / expenses and assets / debts.

Income / Income

Municipal income includes taxes , contributions and fees levied by the municipality itself .

- The taxes levied by a municipality include property tax (A for agriculture, B for all other property ), trade tax , second home tax (since August 2004) and dog tax . The municipality can apply a tax rate ( assessment rate ) to the assessment base for property and trade tax .

- Contributions are cash benefits that are raised by legal entities under public law for the possibility of using public facilities, regardless of whether the benefit is actually used. They are calculated according to the Municipal Tax Act and are due in particular for water supply, sewage or the expansion of local roads and development contributions according to the Building Code for the first-time road system.

- Fees are cash benefits charged by legal entities under public law for the public service actually used. A distinction is made between fees for the use of public facilities ( user fees ) and for an administration service (administration fees ). These include fees for water supply and sewage disposal systems, waste disposal, street cleaning, funeral services, markets, kindergartens, theaters, libraries.

- The municipality's share of income tax is attributed to the municipality of residence of the taxpayer , even if the income is generated outside the municipality; It is therefore the place of residence of the commuters that counts , not their place of work .

- The financial allocations of the respective federal state from the financial equalization are at least as important as the taxes levied. There are allocations for the day-to-day operation of the municipality and for investment measures.

Since 1998 the municipalities have had a share of 2.2% in sales tax revenue , which remains for the federal government after deducting an advance share of 5.63%. The omission of the trade capital tax should be compensated by the municipal share of the sales tax . The revenue from the municipal sales tax share was 2.6 billion euros in 2005. This corresponds to a share of approx. 4.8% of all municipal tax revenues. The municipal share of sales tax is considered a steady and easily calculable source of income for the municipalities.

Local tax determination law

The municipal tax laws of the federal states (e.g. § 9 KAG BW) give the municipalities the right to levy taxes themselves. This must be excise taxes or expense taxes . The municipalities can regulate further consumption or expense taxes through statutes , unless there are already similar taxes under federal or state law. The best known municipal taxes are the second home tax , the dog tax , the amusement tax , the horse tax , the bed tax and the tourist tax .

Expenses / expenses

Operational expenses are all municipal expenses that result from administrative activities (so-called real expenses such as personnel expenses and material costs), including expenses for debt servicing (loan interest and repayments for municipal loans taken out). The operational expenditures are supplemented by the transfer expenditures and form with these the total expenditures. Transfer expenditures serve the redistribution of income policy and are all expenditures that a municipality has to make to its citizens and companies for legal reasons ( social benefits and subsidies for private and public companies) without these having to provide a market economy consideration (see transfer benefit )

The social area comprises transfer payments regulated by federal law, which are to be paid by the municipalities to natural persons based on the provisions of the Social Code (SGB) and other laws . This includes basic security for job seekers (SGB II); the social assistance (SGB XII), including aid for living expenses (§§ 27-40), the basic security in old age and disability (§§ 41 to 46), assistance for health (§§ 47 to 52), integration assistance for disabled people ( Sections 53 to 60), help with care (Sections 61 to 66), assistance in overcoming particular social difficulties (Sections 67 to 69) and assistance in other situations (e.g. help for the blind; Sections 70 to 74); the youth services (SGB VIII); the benefits to war victims ( Federal Supply Act, etc.); Assistance to asylum seekers ( Asylum Seekers Benefits Act ) and other services (e.g. Maintenance Advance Act ). The social sector is a central problem in municipal finances.

Assets and debts

The municipal assets serve municipal tasks ( services of general interest ) and services ( public tasks ) (§ 1 Municipal Property Act (KVG)) and are mostly tangible assets . According to Section 5, Paragraph 1 of the KVG, municipal assets must be used in such a way that their profitable exploitation, effective municipal influence and financial control by the municipalities are ensured and the public purpose is observed. Municipal assets include land , public roads , transport facilities , green and forest areas , supply and disposal systems , schools and kindergartens , sports facilities, administrative and functional buildings or vehicles. The public buildings, streets, traffic routes and other structural facilities must be managed by systematic and planned building management . In addition, the municipal holdings (municipal companies, public companies) also belong to the municipal assets.

Municipal liabilities are made up of cash advances , other municipal loans and all other liabilities including provisions (for components, see debt ratio ). Since 1995, tried to municipalities, over risky financial instruments such as cross-border leasing , foreign currency loans or CMS-Ladder swaps to improve their revenue, have usually had losses suffered.

statistics

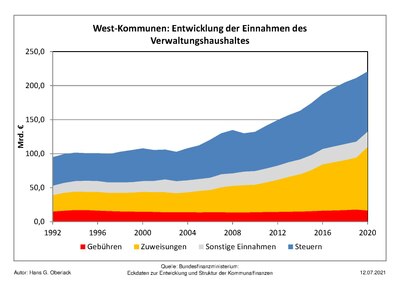

Development of the income of the administrative budget of the West German municipalities

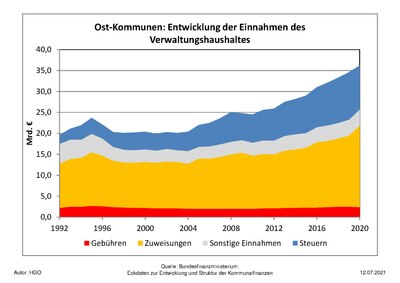

Development of the income of the administrative budget of the East German municipalities

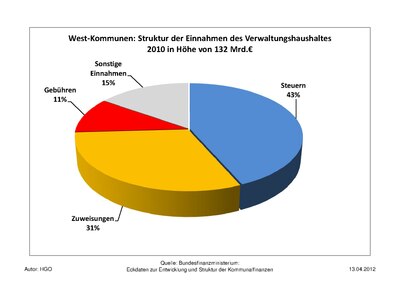

Structure of the income of the administrative budget of the West German municipalities

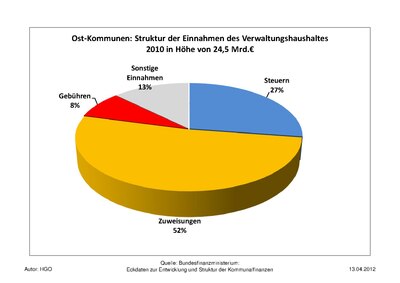

Structure of the income of the administrative budget of the East German municipalities

Municipal finance instruments

In many municipalities, the main task is not to let the gap between declining tax revenues and increasing social spending become too great in order to keep the new debt resulting from this deficit situation sustainable. It is essential to determine key business figures from the municipal financial statements . The situation for municipalities becomes critical when the debt ratio exceeds 70% of total income and / or the interest and repayment service exceeds 20% to 25% of total income or reaches more than 20% of total expenditure ( debt service limit ). Measures to increase income and / or cut expenditure through to austerity policies are available as instruments of local finance . Tight municipal finances exist in municipalities with structural budget balancing , an approved budget security concept or even more so when emergency budget law is imposed. In the ideal case, there is orderly municipal finances in abundant municipalities that are no longer dependent on key allocations from financial equalization.

Shadow debt in municipalities

The problem of government shadow debt continues at the municipal level. In February 2009 , the rating agency Fitch Ratings found that it was missing important financial data such as cross-border leasing and interest rate derivatives for a complete analysis of German municipalities . Fitch considers these financial instruments to be “disadvantageous” for municipalities and assumes that they “have and will have resulted in not inconsiderable contingent liabilities and an additional burden for the already desolate households”. In addition, municipal subsidiaries are outsourced from the municipal core budget and form a shadow budget . The recognizable (explicit) municipal debt must be supplemented by this implicit debt, so that the possible total debt in many municipalities is even higher than the explicit municipal debt.

literature

- Federal Ministry of Finance, BMF (2003a): Report of the “Local Taxes ” working group to the Commission for the Reform of Local Government Finances . Berlin.

- Federal Association of Local Authorities (2003a): Proposal for a modernized trade tax. Berlin.

- Karrenberg, H. (2006): Municipal Finances 2004-2006 - Forecast of the Municipal Central Associations. Berlin.

- Market Economy Foundation (2006): “Tax Code” Commission. Easier, fairer, more social: a comprehensive income tax reform for more growth and employment. Tax policy program. Berlin.

- Zimmermann, H. and Postlep, R.-D. (1980): Assessment criteria for municipal taxes. In: Economic Service. Vol. 60, H. 5, pp. 248-253.

Web links

- Municipal Financial Report 2013 of the Bertelsmann Foundation (PDF)

- Municipal financial report 2012 of the trade union ver.di NRW (PDF)

- haushaltssteuerung.de , portal for public budget and finance management

Individual evidence

- ↑ Stefan Bajohr, Outline State Financial Policy , 2013, p. 59

- ↑ Lending interest is sometimes also included in transfer expenditure, although it represents a consideration to the lender for granting the loan: Volker Häfner, Gabler Volkswirtschaftslexikon, 2013, p. 410

- ↑ The KVG came into force in July 1990 in order to transfer the state-owned assets of the East German municipalities into municipal assets

- ↑ Horst Körner / Sönke Duhm / Monika Huber, Recording and Evaluation of Municipal Assets in Bavaria , 2009, p. 16

- ↑ Fitch Ratings of February 19, 2009, International Public Finance: Germany Special Report, German municipalities - an important role in the federal system , p. 5