Luxembourg leaks

Luxemburg-Leaks ( Luxemburg Leaks or Lux Leaks ) is the name of a financial scandal at the end of 2014. In two phases - "Lux 1" (November 2014) and "Lux 2" (December 2014) - a total of 28,000 pages with 548 binding preliminary notices were published (Advance Tax Rulings) made public by the Luxembourg tax authorities, which they concluded via PricewaterhouseCoopers between 2002 and 2010.

These confidential tax agreements offered 343 international corporations from 82 countries, including Apple , Amazon , eBay Europe S.à rl , Heinz , Pepsi , Ikea and Deutsche Bank , the opportunity to implement “aggressive tax avoidance models ” at the expense of neighboring countries . Your taxes could be reduced to below one percent.

Whistleblowers had passed the documents on to journalists. The evaluation and publication of the " leaked " documents was carried out in international collaboration between several newspapers and broadcasters and the International Consortium of Investigative Journalists (ICIJ).

As a result of the publications, the EU Competition Commissioner Margrethe Vestager announced that she would intensify ongoing investigations into whether European aid law had been violated. The EU Commission then tried to limit tax competition between EU countries. In 2015, a law on the exchange of preliminary tax assessments was passed.

Luxembourg responded to the allegations by pointing out the legality of most of the operations and similar practices in other EU countries such as Great Britain and Germany.

In April and May 2016, the trial against the whistleblower took place in Luxembourg for the transfer of confidential information. Both Luxembourg and the suspended defendants appealed against the judgment of June 2016.

Looking back at the end of 2016, the scandal did not seem to have brought about any change. According to the Eurodad network, the number of tax deals rose even further. In the case of Luxembourg, the number has more than quadrupled.

In January 2017, “German diplomatic cables” reinforced the suspicion that Juncker, as Prime Minister, had secretly blocked measures in the EU Parliament's Code of Conduct Group .

Development of Luxembourg into the world's largest investment center after the USA

From 1980 to 2015, Luxembourg became the world's largest investment center after the USA. From 2006 to 2014, according to the FAZ, the fund volume of the 10,000 Luxembourg funds grew from 1.85 trillion euros to over 3 trillion euros, putting Luxembourg in second place worldwide behind the USA. In terms of the Advance Pricing Agreements (APA), Luxembourg was well ahead of all other countries in Europe in 2014.

According to Gabriel Zucman's calculation approach , the proportion of “ownerless” assets is 50% of the 2.2 trillion euros invested in Luxembourg. Much of that $ 1.1 trillion is likely to be evaded money.

According to estimates by the EU Commission, Member States lose tax revenues of 50 to 70 billion euros annually through tax avoidance by companies.

Assessment of the role of Luxembourg

The historian Christoph Maria Merki sees the following factors as the explanation for the development of Luxembourg into a "financial hub":

- The advantages of a small state are “short distances” and “quick decisions” as well as a good supply of labor from neighboring countries.

- In addition to the multilingual, multicultural atmosphere, the decisive factors were the legal framework, the absolute and criminal compliance with banking secrecy, the high level of legal security and social peace.

- In addition, there was a special "flexibility in the processing of banking transactions", low taxation, low minimum reserve requirements, the "cautious regulatory measures of the legislator" and the "extremely flexible" cooperation of the government with financial experts for the "very short-term" adjustment of the legal framework to new developments .

- According to Merki, the most important and fundamental requirement of this system is Luxembourg's sovereignty , which allows the country to attract foreign banks and investors.

Gabriel Zucman describes Luxembourg as an “economic colony of the international financial industry ”, which forms “the center of European tax evasion ” and “has been paralyzing the fight against this plague for decades”. The secret of success lies in the fact that Luxembourg marketed and sold its own sovereignty by making itself the bailiff of international capital.

The business editor Ulrike Herrmann from the taz commented in 2014 that Luxembourgers are thieves who steal their neighbors' tax money. However, Luxembourg will "never forego operating as a tax haven - because it has nothing else to offer." Like Greece, as a structurally weak country, it lives on " transfers from outside".

In 2014, the satirist Christian Ehring characterized the “nice little” Luxembourg as “ Uli Hoeneß als Land”, and as an Eldorado of tax avoidance by “tax artists”.

Chronicle of financial policy developments (1970s and 1980s)

- 1972: The Bank of Credit and Commerce International (BCCI) registered in Luxembourg is founded.

- 1975: The BCCI becomes a " drug bank "; she buys the Colombian Banco Mercantil in Bogota.

- 1977: Members of the EEC undertake to automatically exchange tax notices, including preliminary notices (“rulings”). None of the member states will implement the resolution by 2015.

- 1982: The Luxembourg branch of Banco Ambrosiano is affected by the bankruptcy of the main bank. Der Spiegel commented that the bankruptcy of the Italian bank caused “considerable excitement” in the small state, “which in recent years has increasingly become one of the most important capital hubs in the western world”. Bundesbank President Karl Otto Pöhl sees the incidents as "a dangerous gap in the international banking network": It is long overdue for the Luxembourg banks to be tied more closely to their mothers. The Banco Ambrosiano and the Luxembourg holding company had "pumped around 1.4 billion dollars into the European money market with the help of guarantee letters from the IOR." The money had gradually disappeared, "as inexplicable as ships in the Bermuda Triangle ; Mailbox companies between Panama and the Bahamas helped collect the billion. "

- July 1988: Manuel Antonio Noriega's assets are transferred from a Luxembourg account.

Under Finance Minister Juncker (1989–1994)

- 1989: Pablo Escobar's drug money is frozen in Luxembourg accounts. The drug lord Jose Rodriguez Gacha also has an account in Luxembourg.

- 1989: RWE transfers profits to its subsidiary in Luxembourg.

- 1991: Jean-Claude Juncker introduces a holding tax of 0.5%.

- 1991: Theo Waigel's announcement of a withholding tax on interest income in Germany leads to a transfer of assets to newly established branches of German banks in Luxembourg.

- July 5, 1991: Bank of Credit and Commerce International (BCCI), a holding company based in Luxembourg, collapses . The banking supervisory authority sees no reason for reproach. Die Zeit quotes Pierre Jaans, the head of the Institut Monetaire: "Banking supervision is a business between honest people, it does not run under the assumption that you are dealing with criminals." Thomas Hanke comments that the EC cannot or does not want to help and Wilfried Kratz. “It does issue common rules for financial institutions, but application is not their business. The EC legislation in matters of financial services is also entirely dominated by the liberalization of the EC market. Only the absolute minimum of new, common rules is to be created. ”However, an employee of the Bundesbank expressed the hope that the trend towards loosening the supervisory rules could be slowed down by the BCCI case. Der Spiegel writes that the Grand Duchy of Luxembourg will once again have to put up with the question of “whether it has a functioning banking supervision at all. And in Washington there is fear of an allegedly long list of American politicians whose protection BCCI is said to have bought. "Only in 2013 will the" pile of broken glass "be finally removed.

- March 1993: Holger Pfahls receives bribe payments into two Luxembourg accounts in the Leuna affair , after he founded several bogus or letterbox companies in 1992 with the help of the Luxembourg trustee Bernard Ewen. In the following years a complex network is built up.

- 1994: The introduction of a withholding tax leads to a flight of capital from Germany amounting to 50 billion marks to Luxembourg.

- January 1994: Searches of German branches of Dresdner Bank for alleged transfer of illegal money.

Under Prime Minister Juncker (1995-2013)

- June 29, 1995: The collapse of the BCCI leads to the adoption of the BCCI follow-up line, which provides for increased supervision, transparency and the exchange of information between national supervisory authorities.

- 1997: A "bribe" run by Ignacio Lopez in the automotive industry collects hundreds of millions of marks from suppliers. Some of the money goes through Luxembourg bogus companies and numbered accounts.

- In 1997, Jeannot Krecké wrote a report on tax fraud in Luxembourg on behalf of Prime Minister Jean Claude Juncker. In the published version, however, a page on the practice of tax rulings in office 6 ( Marius Kohl ) was missing , with which companies could avoid taxes at the expense of neighboring countries. The mirror shows that Claude Juncker claimed not to have known this page. Krecke described this as untrue in September 2015: "I can confirm that I gave Mr. Juncker a public and a personal version of my report in April 1997," wrote Krecke in an email to Spiegel Online . Juncker's “personal version” contained the explosive side, but not the published version, because one wanted to avoid a discussion in Europe.

- 1998–2007: Facilitation payments in the Siemens bribery affair and by other German companies in Brazil are reported by Brazilian MPs.

- 1999: An internal study on tax practices is commissioned by the Code of Conduct Group of the Council of the European Union . The results are never published.

- 2002: Eurostat scandal: Der Spiegel shows that a large part of the profits from corruption in a system for "plundering the EU coffers" was laundered via black accounts, some of which, like Eurostat itself, were based in Luxembourg. The EU Commission is criticized for not wanting to seriously expose the scandal.

- 2003: Agreement with Amazon, according to which its European profits are only offset against a low valuation in Luxembourg.

- 2005: Cum / ex deals, often via Luxembourg, begin to take on a considerable size. The tax refund model will be stopped in 2012 and replaced by cum / cum.

- In 2005, the Volkswagen bribery affair made it clear that there was a "dubious network" of companies in Luxembourg and other countries.

- July 1, 2005: The EU Savings Directive, passed in 2003, comes into force , which only records foreign interest income, but no other forms of investment such as shares; Luxembourg does not apply the directive, strict banking secrecy is maintained, and the directive is in places open to further tax avoidance strategies. Instead of the Savings Directive, Luxembourg levies a flat withholding tax of 20%, from 1 July 2011 35%, and pays three quarters of it anonymously to Germany.

- 2006: The EU wants to tax the profits of companies like Amazon where they are made. In 2008, Juncker succeeded in postponing the application of this rule for Luxembourg to 2015 to 2019. The attempt by Luxembourg to change the text of the treaty itself is prevented by the German Finance Minister Hans Eichel .

- June 9, 2006; After five years of negotiations, the European Commission calls for the abolition of the tax exemption law for holdings that are exempt from income tax under the Luxembourg law of July 31, 1929. The law contradicts Art. 87 (ex 92) of the EC Treaty of 1957.

- 2007: Dolce Gabbana scandal; Tax evasion in 2004 and 2005 through the front company "Gado" in Luxembourg.

- May 11, 2007: Law aimed at managing the private wealth of natural persons, Family Wealth Management Company (SPF). In order to ensure absolute “tax neutrality”, an SPF is not subject to corporate income tax, municipal trade tax or wealth tax. Because of this tax exemption, the double taxation agreements concluded by Luxembourg are not applicable to an SPF.

- January 1, 2008: Patent and license box, a tax exemption of 80 percent from the use or the right to use intellectual property .

- March 2009: Luxembourg representatives react angrily when Luxembourg is placed on the OECD's "gray list of tax havens " at the G20 meeting in London, despite a promise to relax its banking secrecy . Juncker forbids Germany from interfering with the internal affairs of Luxembourg and compares Franz Müntefering's statements with the Nazi era .

- April 2009: At the urging of the major industrialized and emerging economies, the OECD introduces black, gray and white lists of countries to control tax evasion .

- April 2009: In Germany, the bill by Finance Minister Peer Steinbrück against tax evasion via tax havens - with an obligation to provide information about business contacts to tax havens - threatens to fail in the grand coalition due to reservations by the CDU / CSU, as Steinbrück take the "honest taxpayer hostage and with him To press conditions, bureaucracy and harassment ”.

- May 2009: The German Finance Minister Peer Steinbrück compares Luxembourg as a tax haven with Burkina Faso and is therefore reprimanded by Jean Asselborn for arrogance. Asselborn complains to Foreign Minister Frank-Walter Steinmeier about Steinbrück.

- July 8, 2009: By concluding twelve double taxation agreements , Luxembourg is the first country to be removed from the gray list again, even if an agreement with Germany has not yet been reached. Germany is calling for changes compared to the previous twelve agreements.

- October 13, 2010: Theft of the Lux Leaks documents by Antoine Deltour, charges by PricewaterhouseCoopers (PwC) against unknown persons.

- December 31, 2010: Luxembourg, under pressure from the Commission, renounces the continued application of the 1929 Law on Luxembourg tax breaks for financial holdings. A transitional arrangement exists for the companies concerned until January 1, 2011, before they become fully taxable.

- Autumn 2011: Siemens receives information about a black account for bribery payments in Luxembourg; the investigation into the bribe scandal begins.

- 2012: The tax loophole for CumEx deals is closed seven years after its introduction and replaced by Cum-cum .

- May 2012: In France, based on information from Deltours, France 2 broadcasts a report on tax evasion practices by PwC that goes unnoticed .

- October 30, 2012: The assets of the Nigerian dictator Sani Abacha in Luxembourg front companies are confiscated.

Under Finance Minister Gramegna (from 2013)

- The US Bureau of Economic Analysis reported $ 416 billion in direct investments by US companies in 2013 , 80 percent of which from holding companies .

- January 1, 2014: Luxembourg undertakes to report interest income, from 2017 also other income.

- End of April 2014: Examination of the Lux Leaks documents from 2010

- May 2014: Grand Duke Henri of Luxembourg inaugurates the Freeport , a depot near the airport for the tax-free storage of property, works of art (avoidance of VAT when buying) to gold bars (e.g. due to inheritance tax).

- November 2014: Publication of the Lux Leaks documents.

- November 1, 2014: Jean-Claude Juncker becomes President of the European Commission . A vote of no confidence requested against him finds no majority in the European Parliament on November 27th .

- December 2014: Whistleblower Antoine Deltour was charged with divulging trade secrets.

- February 24, 2015: Raid on the German Commerzbank.

- April 26, 2016: Deltour, Halet and Perrin trial started (see this section ).

- January 1, 2017: Based on the leaked documents, the Guardian accused Juncker of secretly blocking EU efforts as prime minister to address multinational corporate tax avoidance.

.jpg)

The published documents

Sighting and publication

At the end of April 2014, 80 journalists from 26 countries began sifting through almost 28,000 pages of confidential documents, most of which came from the holdings of the consulting firm PricewaterhouseCoopers (PwC) Luxembourg.

The documents are tax agreements, tax returns and other documents. The screening and research was coordinated internationally by the International Consortium of Investigative Journalists (ICIJ) and funded by the Center for Public Integrity . PricewaterhouseCoopers said most of the documents were stolen in 2010. At that time a complaint was filed against unknown persons.

LuxLeaks 1

At the beginning of November 2014, the journalists involved published the results of the document viewing and research in a large number of European media . At the same time, the ICIJ published some of the documents on the Internet: 548 tax agreements and 16 other documents such as B. Tax returns.

In addition to the NDR and WDR , the newspapers Süddeutsche Zeitung (Germany), Tages-Anzeiger (Switzerland), The Guardian (Great Britain) and Le Monde (France) as well as dozens of other media were involved in the document evaluation and research .

Journalists or media companies from Luxembourg were not involved in the publications.

LuxLeaks 2

On December 9, 2014, ICIJ published the names of around 30 other large corporations that had benefited from Luxembourg's tax avoidance models. This second wave is known as “LuxLeaks 2” because it complements the first publications from November 2014.

Tax agreements

The published 548 tax agreements between Luxembourg authorities and international groups were drawn up by PricewaterhouseCoopers (PwC) between 2002 and 2010. PwC assured the companies in writing that the tax models would be approved by the Luxembourg authorities. The basis of the tax models used by PricewaterhouseCoopers is, among other things, the 80 percent tax exemption applicable in Luxembourg for profits from intellectual property.

Upon request, the Luxembourg Ministry of Finance will issue an official confirmation in advance that the tax structure will be examined benevolently when the tax return is submitted and that it will be taxed at a certain (low) tax rate. These tax constructs are legal in Luxembourg, but in individual cases they may violate foreign tax law. B. as tax-motivated transfer pricing . A group can make a proposal for the structure of a holding company to the Luxembourg authorities even if it does not yet exist. In this way a company can find out how the tax assessment will be composed in the future. If the proposed structure is not accepted, it can be changed. Once a holding structure has been approved, the approval is valid for five years.

The tax agreements include offshore investments and the like. a. in Luxemburg. These complex models mean that profits that are generated outside of Luxembourg are shifted to Luxembourg because only a fraction of them have to be taxed there. The British investigative journalist and former tax investigator Richard Brooks comes to the conclusion that the models mostly run as follows (here using Pearson plc as an example ):

- A group gives capital to its Luxembourg branch (a).

- This makes a capital contribution to a subsidiary in Luxembourg (b),

- This subsidiary lends the money to a group subsidiary z. B. in the USA, Germany etc. and receives a large amount of loan interest (c).

In consultation between PwC and Marius Kohl from the Luxembourg tax administration, the non-interest-bearing intra-group money shift (a) was treated as a fictitious loan, although there was no loan agreement and no interest was paid. Taxable income in Luxembourg therefore only arose in the amount of the loan interest from (c) minus a notional loan interest from (a). This leads to the result:

- In Luxembourg, only a fraction of the loan interest actually paid (here 0.06%) is taxed as taxable income.

- In the USA, Germany etc., the loan interest reduces the taxable income in full (100%).

Another variant is the postponement of licenses within the company and the subsequent payment of license fees to a financial subsidiary of the same company.

In many cases, the company's economic activity and personnel presence in Luxembourg is very low, although hundreds of millions of euros are managed there. For example, a single popular address, 5, rue Guillaume Kroll , is home to more than 1,600 companies. The E.ON SE, headquartered in Dusseldorf for example, had, according to the balance sheet from 2011 in its Luxembourg subsidiary company " Dutch Delta Finance S.à rl " except its CEO not employees, but managed several billion euros. In 2008, around 33 billion euros were accounted for as additions. The managing director, Paul de Haan, runs several companies in Luxembourg. According to NDR, his job is “to give company offshoots in Luxembourg their own presence”. The business addresses of Dutchdelta and de Haans consulting company, Intruma Corporate Services , are identical (Boulevard Prince Henri 17). E.ON let it be known in writing that Dutchdelta was working independently and that all business matters would also be dealt with on site in the Luxembourg branch. The tax investigation in Frankfurt am Main is now looking into the question of whether Dutchdelta is a mailbox company .

- Contact person from PwC

PwC had a direct contact person - Marius Kohl - the head of the Luxembourg tax office “Sociétés 6”. Kohl was responsible for assessing and approving the "rulings", as the agreements between the state of Luxembourg and international corporations are called. PwC's consultants personally presented the company's plans to Kohl on behalf of their customers. As a rule, a written application was then submitted after one or two meetings. This was then approved by Kohl on the same day. The Luxembourg leaks show that Kohl was solely responsible for processing during his 22-year term in office and that at the top 54 applications were positive on a single day. Kohl retired in 2013.

Participating companies

Big Four

In 2013 the “ Big Four (auditing firms) ” were the subject of an investigative commission of the British Parliament. The commission found that, among other things, PwC sells tax models with a 75 percent risk of being classified as non-compliant. The assessment is based on a statement by a senior consultant at PwC.

Large corporations

According to media reports, among others, Google , Apple , Amazon , FedEx , IKEA , PepsiCo , Heinz , Procter & Gamble and the DAX groups Deutsche Bank , E.ON and Fresenius Medical Care benefited from the tax agreements .

- Deutsche Bank is based in Luxembourg and other tax havens with fund companies. Real estate transactions in Europe are processed through the funds without incurring significant taxes.

- The energy company E.ON and the health care company Fresenius Medical Care are granting loans to other subsidiaries outside of Luxembourg through subsidiaries in Luxembourg. Fresenius Medical Care itself stated that it would save almost one million euros in taxes each year. E.ON's subsidiaries transferred interest to Luxembourg, which reduced the profits of companies outside Luxembourg and thus the company's overall tax burden.

Consequences

In addition to legality, Prem Sikka , Professor of Accounting at the University of Essex , also questions the credibility of the companies involved in view of the procedures that have become known. Many companies have published reports on “ Corporate Social Responsibility ” without discussing their strategies for tax avoidance at the same time. Luxembourg leaks reveal the "organized hypocrisy" of modern companies.

Sikka described the activity of tax advisory firms as an expression of an “organized tax avoidance industry” dominated by four companies: Deloitte, Pricewaterhouse Coopers, KPMG and Ernst & Young (“ Big Four ”).

In the course of the discussion triggered by the publication, the recently appointed President of the European Commission Jean-Claude Juncker came under criticism. Juncker was Minister of Finance from 1989 to July 2009 and Prime Minister of Luxembourg from 1995 to December 2013. The EU Commission is investigating tax practices and tax laws for which Juncker was responsible in his former offices. When he took up his new office, Juncker had also announced that he wanted to restore the credibility of European politics; the affair, however, often called his own credibility into question. Against the background of the publications about the Luxembourg leaks, it was discussed whether this situation would result in a conflict of interest for the EU Commission President.

Luxembourg's reaction

The Luxembourg politician Frank Engel , member of the EU Parliament for the ruling party ( CSV ), summed up the problem in an interview with BBC Radio 4: “We don't like to be called a 'tax haven'. We allow multinational corporations to settle with us to pay symbolic taxes. If we don't do that, others will. "

Luxembourg points out that most of the practices are legal and at least as widespread in other EU countries and around the world, notably in the UK and Germany. The Global Financial Secrecy Index shows that Luxembourg lags far behind other countries in terms of the volume of financial transactions. Markus Meinzer estimates the share of untaxed investments in Germany at three trillion euros.

The Luxembourg Prime Minister Xavier Bettel also takes the view that what happened in Luxembourg is legal.

The Tax Justice Network (TJN), on the other hand, considers it nonsense for various reasons to call these tax-saving models “legal”.

- First, the claim that Luxembourg has not broken any international tax laws is nonsensical because there is no international "world financial order" and no "world tax authority". There are simply no laws that Luxembourg can break. Without law there is no breach of law. The Luxembourg practices are therefore neither illegal nor legal - they happen in a lawless area . Only the OECD can draw up guidelines, which, however, cannot be compared with laws.

- Second, Luxembourg has developed a business model from selling tax agreements that international companies use to circumvent international tax guidelines and national tax laws. It is therefore a very disturbed view of things to say that Luxembourg has not violated any international tax rules.

- Thirdly, the Luxembourg Leaks have shown that Luxembourg not only sells tax models, but also their secrecy.

Investigations by German tax offices

At the same time as the Luxembourg Leaks, specialists from the tax authorities in North Rhine-Westphalia and employees of the “Investigation Group for Organized Crime and Tax Evasion” (EOKS) investigated tax evasion by German private individuals and companies via Luxembourg. The focus of the investigation was Commerzbank, which was searched in February 2015. In 2014, Luxembourg rejected a request from the German authorities for mutual legal assistance.

Measures within the EU on corporate taxation

European Commission plans

Tax transparency package March 2015

The Commission's first act was a tax transparency package presented by Pierre Moscovici on March 18, 2015. It mainly contained a system of automatic exchange of information on advance tax ruling between the tax administrations of the Member States. From the outset, NGOs and Members of Parliament considered these measures to be inadequate as no publication of the tax agreements is expected.

The remarks on the implementation of the package cite the events surrounding Luxleaks as the main motive of the Commission's resolution. Therefore, some politicians critical of the EU fear that the Commission will use LuxLeaks as an instrument to enforce tax harmonization.

In October 2015, European finance ministers assessed the automatic exchange of information without informing the European Commission or the public of the results of their deliberations.

Violation of EU state aid rules

The European Commission examines in three cases ( Starbucks , Apple , Fiat ) whether European law has been violated (competition and state aid law, there is no harmonized European corporate tax law), and in the Apple case the Irish government has similarly lax laws in their area for tax avoidance, asked to collect the outstanding taxes from Apple.

On October 21, 2015, the EU Commission decided that the tax breaks granted by the Netherlands and Luxembourg to multinational corporations constituted illegal aid. The underpaid taxes have to be paid in arrears, for example the financial subsidiary of Fiat in Luxembourg has to pay 20 to 30 million euros. EU Competition Commissioner Margrethe Vestager said: "Tax rulings that artificially reduce a company's tax burden are not in line with EU state aid rules" because they penalize other companies that pay reasonable taxes.

Action plan June 2015 / January 2016

A second resolution took place on June 17, 2015 with the submission of the action plan "for a fundamental reform of corporate taxation in the EU". The aim of the measures is to “make the tax framework for companies in Europe fairer, more efficient and more growth-friendly and thus to improve them considerably.” Pierre Moscovici said of the introduction of this action plan “Corporate taxation in the EU needs radical reform [ and] everyone must pay their fair share ".

The plan is to renew the Common Consolidated Corporate Tax Base four years after the previous attempt was rejected by member states. Part of the plan are also measures to enforce effective taxation of companies in the countries where their profits are made. The Commission also listed the top 30 tax havens outside the EU. NGOs expressed doubts that the plan would actually eliminate profit shifting by multinational firms. They also emphasized the lack of will to tackle the problem quickly.

The Commission adopted the Action Plan on January 27, 2016, which included measures to combat tax avoidance, including the automatic exchange of important information on the activities of multinationals. However, to implement this plan, it must be accepted by all member states without exception. The action plan has already been assessed by tax associations as being too weak a means of combating tax avoidance.

A new plan was presented on April 12, 2016. A study by the European Parliament assumes tax losses of between 50 billion and 70 billion euros.

In June 2016, the member states agreed on a joint approach against tax avoidance methods. However, agreement could only be reached by adopting exceptions and extending the time for implementation, which will likely weaken the effectiveness of the agreement.

Common tax base October 2016

In October 2016, the Commission proposed a common tax base for all companies operating in the EU.

Actions by the European Parliament

A special committee of the EU Parliament (“TAXE committee”) was set up to investigate the processes . A committee of inquiry , which, in contrast, would have been given more formal rights and had better access to documents from the member states, did not come about.

The special committee was set up on February 12, 2015 and worked for half a year. According to one member, during the first two months it was discussed which files should be requested. An internal study from 1999, in which the Council of the European Union investigated unfair tax practices, was not made available to the committee. His rapporteur, Michael Theurer , ruled on May 6, 2015 that the work of the special committee was being reduced to absurdity.

At the beginning of September 2016, on the initiative of German MP Fabio De Masi , over 100 members of the EU Parliament declared their solidarity with the two whistleblowers Deltour and Halet in an open letter.

Criminal proceedings in Luxembourg against whistleblowers and whistleblowers

accusation

In December 2014 it was announced that the public prosecutor would bring charges against Antoine Deltour.

On April 23, 2015, the Luxembourg judicial authority announced that the prosecutor was bringing charges against three French people: Edouard Perrin, Antoine Deltour and Raphaël Halet. Perrin was the first journalist to uncover the affair in May 2012 - in the program Cash Investigation on France's largest public broadcaster , France 2 . Deltour and Halet are former employees of the auditing company PwC.

The allegations include data theft and disclosure of trade secrets . The accused faced prison sentences of up to ten years, while the question of political responsibility remained unresolved and those responsible for politics had little to fear.

The ICIJ, which coordinates the research of the journalists involved in the Luxembourg leaks, strongly condemned the decision of the investigating judge.

Procedure

One year later, on April 26, 2016, the proceedings were opened. Deltour, who entered the court to the applause of dozens of supporters, was the "main source" for journalist Perrin, according to the prosecutor. Deltour was initially threatened with a fine and up to ten years in prison.

support

Supporters help him financially and collected more than 175,000 signatures for him in a campaign on the Internet. Among the many prominent supporters of the accused was France's Finance Minister Michel Sapin , who declared in the French parliament on April 26, 2016 that Deltour had “ defended the common good ” and expressed his solidarity with the whistleblower: “It is thanks to him that we were able to end this opaqueness that was hiding the exact tax situation of a number of large companies in Luxembourg from European countries, ”added Sapin to the applause of MEPs.

judgment

On May 10, 2016, the public prosecutor's office demanded that Deltour and Halet be fined 18 months in prison; a fine was requested for Perrin. On June 29, 2016, Deltour were sentenced to one year and Halet to nine months in prison and a fine each (Deltour: 1,500 euros). The sentences were suspended.

At the same time, the court determined that if they both committed the same act today, they would be protected as whistleblowers due to a change in the law and would therefore not be convicted. Perrin was acquitted.

Appeal process

Both Deltour and Halet and the Luxembourg public prosecutor have appealed the judgment. The Luxembourg judiciary justifies its decision mainly with the acquittal for Perrin. In March 2017, an appeals court reduced the sentence. Deltour was sentenced to six months probation and a fine of 1,500 euros, Halet received a fine of 1,000 euros. Both appealed again. On January 11, 2018, the Court of Cassation in Luxembourg lifted the suspended sentence against Deltour. The lesser sentence for Halet, however, was maintained.

Balance sheet 2016 and further development

According to a report by Eurodat, the number of tax agreements in Europe, including with Luxembourg, has continued to rise massively. From 547 in 2013, the number had grown steadily to 1,444 deals by the end of 2015. In the case of Luxembourg, the deals would have more than quadrupled (from 113 to 519).

The European Commission criticized the report. These are not so-called sweetheart deals.

On January 1, 2017, the Guardian accused Juncker, on the basis of "German diplomatic cables", of secretly blocking EU efforts as prime minister to tackle tax avoidance by multinational corporations:

"Years 'worth of confidential German diplomatic cables provide a candid account of Luxembourg's obstructive maneuvers inside one of Brussels' most secretive committees."

In the code of conduct group on business taxation, which began its work in 1997, efforts to restrict tax avoidance by the actions of some of the smallest members of the EU were regularly delayed, watered down or derailed under the leadership of Luxembourg. Among the proposals rejected by Luxembourg were, for example

- Plans for a peer review of corporate tax policies

- an investigation into hybrid mismatches

- Exchange between the countries on tax agreements with large corporations

The presentation of Luxembourg's obstructive policy was also prevented: in a communication, Luxembourg representatives said they would reject any proposal to publish Luxembourg's arguments in the committee.

"It is impressive to see how some member states present themselves to the outside world as advocates [international tax reform], and at the same time to see how they really behave in EU discussions when they are protected by confidentiality."

See also

- List of tax data leaks

- Panama Papers - April 2016

- Paradise Papers - November 2017

- Swiss Leaks - February 2015

- Offshore Leaks - April 2013

- Liechtenstein tax affair - February 2008

literature

- Rainer Falk: On the debate about tax havens: The Luxembourg case. Questions from a development perspective. Published by the Cercle de Coopération des ONG de Développement au Luxembourg asbl 13, av Gaston Diderich L-1420 Luxembourg tél: +352 - 26 02 09 11 [email protected] www.cercle.lu Luxembourg, July 2009.

- Walther, Olivier / Christian Schulz: Luxembourg financial center. From “tax haven” to investment fund capital. In: Geographische Rundschau, vol. 61, issue 1/2009, pp. 30–35.

Web links

- The documents can be viewed on the ICIJ website, sorted by sector and company:

- NDR film on Luxembourg leaks: ringing the bell for the mysterious billion-dollar company

- Luxleaks in the newspaper Luxemburger Wort : LuxLeaks, tax dumping in the Grand Duchy

Individual evidence

- ↑ a b c d e Explore the Documents: Luxembourg Leaks Database . In: International Consortium of Investigative Journalists . ( icij.org [accessed October 27, 2016]).

- ↑ Here's A Full List Of Companies That Allegedly Have Shady Tax Deals With Luxembourg . In: Business Insider . ( businessinsider.com [accessed October 27, 2016]).

- ↑ https://www.tagesschau.de/ausland/luxleaks-process-101.html

- ^ NDR: Luxemburg Leaks: Criticism of Juncker is growing , November 7, 2014

- ↑ a b c Number of EU tax deals increases massively . ( tagesspiegel.de [accessed December 19, 2016]).

- ↑ Simon Bowers: Jean-Claude Juncker blocked EU curbs on tax avoidance, cables show . In: The Guardian . January 1, 2017, ISSN 0261-3077 ( theguardian.com [accessed February 6, 2017]).

- ^ A b Bastian Brinkmann, Christoph Giesen, Frederik Obermaier, Bastian Obermayer, Klaus Ott: Luxembourg Leaks: Trouble in the tax fairytale land . In: sueddeutsche.de . ISSN 0174-4917 ( sueddeutsche.de [accessed April 10, 2016]).

- ↑ Michael Stabenow, Gerald Braunberger, Philip Plickert: Farmers, steelworkers and bankers: How Luxembourg became the richest country in Europe . In: Frankfurter Allgemeine Zeitung . November 14, 2014, ISSN 0174-4909 ( faz.net [accessed April 16, 2016]).

- ↑ http://www.eurodad.org/SweetheartTaxDealsTrendingInEU

- ↑ Economist: Tax havens continue to boom. In: derStandard.at. Retrieved April 16, 2016 .

- ↑ http://gabriel-zucman.eu/files/press/201407WirtschaftsWoche.pdf

- ↑ limited preview in the Google book search

- ↑ Gabriel Zucman: Tax havens: Where the prosperity of nations is hidden . Suhrkamp Verlag, 2014, ISBN 978-3-518-73788-0 ( google.com [accessed on May 17, 2016]).

- ↑ http://www.taz.de/!5029278/

- ↑ https://www.ndr.de/fernsehen/sendung/extra_3/Ehring-zur-Steueroase-Luxemburg,extra8484.html

- ↑ https://www.ndr.de/fernsehen/sendung/extra_3/Satiresendung,sendung303274.html

- ↑ a b "Greed, theft, lawlessness" . In: Der Spiegel . No. 33 , 1991, pp. 86-88 ( online ).

- ↑ Banks: Danger from Luxembourg . In: Der Spiegel . tape July 29 , 1982 ( spiegel.de [accessed April 13, 2016]).

- ↑ A piece from the madhouse . In: Der Spiegel . tape 32 , August 9, 1982 ( spiegel.de [accessed April 13, 2016]).

- ↑ a b Dirty money, clean helpers . In: Der Spiegel . tape February 9 , 1992 ( spiegel.de [accessed April 16, 2016]).

- ↑ Hans-Lothar Merten: Tax evasion: The billion dollar business with black money. An insider unpacks . Linde Verlag GmbH, 2012, ISBN 978-3-7093-0481-5 ( google.com [accessed on April 16, 2016]).

- ^ BCCI collapse: out of control . In: The time . ISSN 0044-2070 ( zeit.de [accessed April 13, 2016]).

- ^ BCCI collapse: out of control . In: The time . ISSN 0044-2070 ( zeit.de [accessed April 13, 2016]).

- ↑ 25 years ago: The BCCI bankruptcy shook Luxembourg. In: Wort.lu. Retrieved April 13, 2016 .

- ^ SPIEGEL ONLINE, Hamburg Germany: Pfahls trial: Judges roll up the scandals of the Kohl era. In: SPIEGEL ONLINE. Retrieved April 26, 2016 .

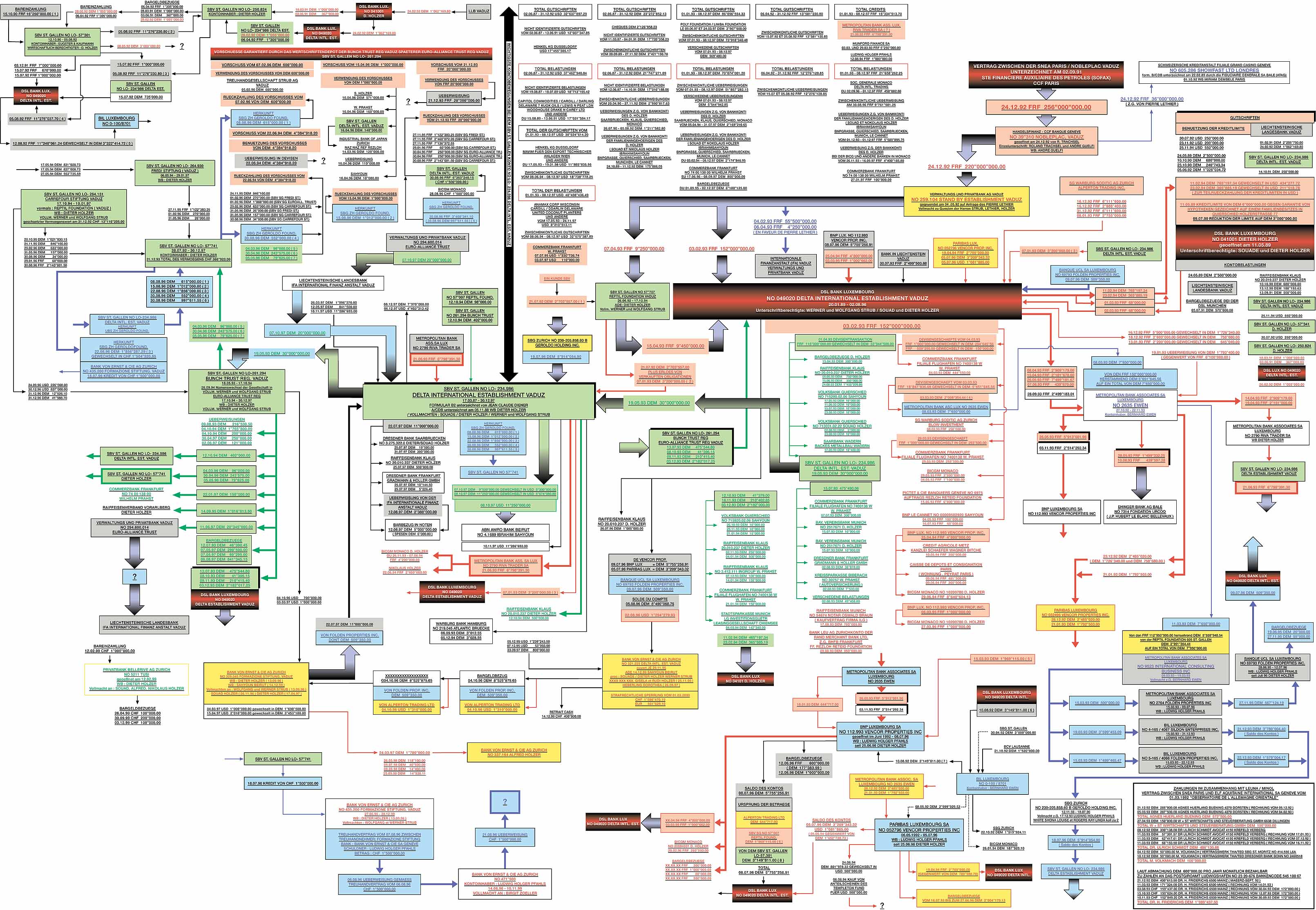

- ↑ http://investigativ.org/wp-content/uploads/2013/07/Geldwaesche-Grafik.jpg

- ↑ 3.5.1.2.2 - Affair Elf Aquitaine / Leuna: Money laundering graphic. In: images.google.de. Retrieved April 26, 2016 .

- ↑ FOCUS Online: Welcome. In: FOCUS Online. Retrieved April 26, 2016 .

- ↑ Thomas Göbel: Framework conditions of an attractive financial center and their possible changes. diplom.de, 2001, ISBN 978-3-8324-3803-6 , p. 6 ( limited preview in the Google book search).

- ^ Kai-Oliver Knops: Handbook on German and European banking law . Springer Science & Business Media, 2008, ISBN 978-3-540-76644-5 , pp. 2195 ( limited preview in Google Book search).

- ^ Dietmar Hawranek, Richard Rickelmann: affairs: commission for the network . In: Der Spiegel . No. 8 , 1997, pp. 82-87 ( Online - Feb. 17, 1997 ).

- ↑ SPIEGEL ONLINE, Hamburg Germany: Luxembourg tax scandal: Juncker is said to have lied to parliament - SPIEGEL ONLINE - Economy. Retrieved February 6, 2017 .

- ↑ http://www.sven-giegold.de/2016/luxleaks-tax-rulings-chronology-events/

- ↑ Luxleaks - "The Enlightenment Is Sabotaged". In: Deutschlandfunk. Retrieved May 6, 2016 .

- ↑ SPIEGEL ONLINE, Hamburg Germany: Self-service in Luxembourg: EU Commission fails in the Eurostat corruption scandal. In: SPIEGEL ONLINE. Retrieved April 16, 2016 .

- ^ A b c Christoph Pauly: Investment luxury castle for Luxembourg . In: Der Spiegel . tape 44 , October 27, 2014 ( spiegel.de [accessed April 16, 2016]).

- ^ Klaus Ott Berlin: Cum-Ex-Shops: State gave away money to millionaires . In: sueddeutsche.de . ISSN 0174-4917 ( sueddeutsche.de [accessed on April 16, 2016]).

- ↑ Michael Fröhlingsdorf, Dietmar Hawranek, Sven Röbel: Volkswagen: Das Schattenreich . In: Der Spiegel . No. 30 , 2005, pp. 72-75 ( online - 25 July 2005 ).

- ↑ a b c FOCUS Online: Last Refuge. In: FOCUS Online. Retrieved April 26, 2016 .

- ↑ a b Luxembourg Leaks: "When things get serious, you have to lie". In: www.wiwo.de. Retrieved April 16, 2016 .

- ↑ The information channel of real life: Tax-free - How corporations plunder Europe's coffers. April 8, 2014, accessed April 16, 2016 .

- ↑ Art. 87 EC (ex-Art. 92) - dejure.org. In: dejure.org. Retrieved May 16, 2016 .

- ^ Treaty establishing the European Economic Community (Rome, March 25, 1957). In: cvce.eu. Retrieved May 16, 2016 .

- ↑ L'essentiel: L'essentiel Online - 343 million fine for Dolce & Gabbana - economy. In: L'essentiel in German. Retrieved April 16, 2016 .

- ↑ New law grants 80 percent tax exemption for income from intellectual property. Retrieved May 18, 2016 .

- ↑ a b n-tv news television: Removed from OECD list: Luxembourg washes clean. In: n-tv.de. Retrieved April 26, 2016 .

- ↑ a b Dispute over tax havens: Luxembourgers are foaming because of Steinbrück's Africa comparison. In: SPIEGEL ONLINE. Retrieved April 10, 2016 .

- ↑ Controversy over tax havens: Juncker forbids "German powerhouse" . In: The time . ISSN 0044-2070 ( zeit.de [accessed April 10, 2016]).

- ↑ a b Gray list: Switzerland is no longer a tax haven . In: The time . September 24, 2009, ISSN 0044-2070 ( zeit.de [accessed April 26, 2016]).

- ↑ The black list of tax havens is empty again . In: Welt Online . April 7, 2009 ( welt.de [accessed April 26, 2016]).

- ↑ a b Luxembourg deleted from “gray list”. In: Wort.lu. July 8, 2009, accessed April 26, 2016 .

- ↑ Siemens' antitrust affair in Brazil: Secret account in Luxembourg starts internal investigations . In: sueddeutsche.de . ISSN 0174-4917 ( sueddeutsche.de [accessed on February 6, 2017]).

- ↑ Luxprivat: The Geneva judiciary has illegal money confiscated in Luxembourg. In: www.luxprivat.lu. Retrieved April 16, 2016 .

- ↑ Bastian Brinkmann, Hans Leyendecker, Bastian Obermayer, Klaus Ott: Investigations into tax evasion: Strike against Luxemburg - raid on Commerzbank . In: sueddeutsche.de . ISSN 0174-4917 ( sueddeutsche.de [accessed on May 6, 2016]).

- ↑ a b c Simon Bowers: Jean-Claude Juncker blocked EU curbs on tax avoidance, cables show . In: The Guardian . January 1, 2017, ISSN 0261-3077 ( theguardian.com [accessed February 5, 2017]): "It is impressive to see how some member states present themselves outwardly as proponents of [international tax reforms] and at the same time to watch how they actually behave in EU discussions, protected by confidentiality. "

- ↑ a b c d e Bastian Brinkmann: This is how Luxemburg-Leaks was researched. In: Süddeutsche Zeitung. November 6, 2014, accessed November 6, 2014 .

- ^ The Guardian, Luxembourg tax files: how tiny state rubber-stamped tax avoidance on an industrial scale

- ↑ The-data-already-disappeared - 2010. In: tageblatt.lu. November 6, 2014, accessed November 6, 2014 .

- ↑ ( Reuters / mol): German companies save billions through tax tricks. In: The world . November 6, 2014, accessed November 9, 2014 .

- ↑ taz, Tax Oasis Luxembourg - The Money of Others

- ↑ a b ICIJ, Key findings

- ↑ ICIJ, Leaked Documents Expose Global Companies' Secret Tax Deals in Luxembourg , November 5, 2014

- ^ A b Wall Street Journal, The man who made Luxembourg a tax haven

- ^ Richard Brooks, The Great Tax Robbery , Oneworld Publications, 2013, ISBN 978-1-78074-102-4 , Chapter: At home with the tax-dodgers

- ^ SZ: This is how the corporations in Luxembourg trick , November 6, 2014

- ^ A b Süddeutsche Zeitung, Luxembourg leaks on Eon Windige Kredite , November 7, 2014

- ↑ Intruma Corporate Services S.à rl , “Our services comprise the set up, management and administration of intermediate Luxembourg holding and finance companies for use by international corporations”, accessed on November 11, 2014

- ↑ NDR, How E.ON Tears Tax Holes worth millions , November 6, 2014

- ↑ Süddeutsche Zeitung, Luxemburg-Leaks - Why is Luxemburg a “magical fairytale land”?

- ↑ Tagesanzeiger, Luxembourg's billions in discounts for large corporations

- ↑ Big accountancy firms have a human rights problem , Prem Sikka, Professor of Accounting, Essex Business School at University of Essex, June 30, 2014

- ↑ Die Zeit, tax haven Luxembourg - now even more so , 6 May 2013

- ^ Die Süddeutsche, Luxemburg-Leaks - Tax haven-hopping with Ikea , November 11, 2014

- ↑ essex.ac.uk: University of Essex :: Essex Business School :: Academic Staff :: Professor Prem Sikka , accessed November 10, 2014

- ^ The Conversation : Luxembourg leaks reveal the organized hypocrisy of the modern corporation. from November 10, 2014.

- ^ Walter Wüllenwebe: "Luxemburg Leaks". How Google, Apple and Co trick the system . In: Stern. November 7, 2014. Retrieved November 18, 2014.

- ↑ Matthias Krupa : A giant European . In: The time. No. 47/2014. Page 10.

- ↑ Süddeutsche Zeitung, Juncker versus Juncker

- ^ NDR, Luxemburg Leaks: Criticism of Juncker is growing

- ↑ BBC Radio 4, Today Show, November 27, 2014

- ↑ http://www2.weed-online.org/uploads/schattenfinanzzentrum_deutschland.pdf

- ↑ https://netzwerksteuerrechte.files.wordpress.com/2015/11/deutschland-schattenfinanzindex-20151.pdf

- ↑ Financial Secrecy Index - 2015 Results ( Memento of December 8, 2015 in the Internet Archive )

- ↑ AltrimentiVideo: Markus Meinzer - Tax haven Germany. December 10, 2015, accessed February 6, 2017 .

- ↑ Meinzer, Markus: Tax haven Germany: Why many rich people don't pay taxes here. 2nd edition 2016. 288 pp. ISBN 978-3-406-66697-1

- ↑ Tax Justice Network, PWC and Luxembourg: no, this wasn't 'legal' behavior

- ↑ Tagesschau, suspected tax evasion via the Luxembourg raid at Commerzbank ( memento of February 24, 2015 in the Internet Archive ), February 24, 2015

- ↑ Benjamin Fox: EU plans 'revolution' on sweetheart tax deals . March 31, 2015. Accessed July 7, 2015.

- ↑ James O'Brien: MEPs unconvinced by commission's 'revolutionary' EU tax transparency proposals . In: The Parliament Magazine , March 31, 2015. Retrieved July 7, 2015.

- ↑ European Commission's Tax Transparency Package keeps tax deals secret . In: European Network on Debt and Development . March 18, 2015. Retrieved July 7, 2015.

- ^ Will Fitzgibbon: 'Fundamental change' in EU tax rules after LuxLeaks . In: International Consortium of Investigative Journalists . March 18, 2015. Retrieved July 7, 2015.

- ↑ Tax Transparency Package: Commission will use LuxLeaks to push for harmonization, ECR Group fears . March 24, 2015. Retrieved July 7, 2015.

- ↑ Alex Pigman: EU agrees greater transparency on tax deals after LuxLeaks scandal . October 6, 2015.

- ↑ New EU transparency rule to close corporate tax loophole . In: ICIJ . October 8, 2015. Accessed October 27, 2015.

- ↑ European Commission, press release , June 11, 2014

- ↑ EU insists on billions in arrears from Apple. In: Spiegel Online. February 5, 2017. Retrieved February 5, 2017 .

- ^ FAZ, Tax deals from Starbucks, Amazon and Co are illegal , October 21, 2015

- ↑ Press release of the European Commission of June 17, 2015: Commission presents an action plan for fairer and more efficient corporate taxation in the EU

- ^ Tax Justice Network, European Commission half measures will exacerbate profit shifting

- ^ Commission presents Action Plan for Fair and Efficient Corporate Taxation in the EU . European Commission. June 17, 2015. Retrieved July 7, 2015.

- ^ Commission to propose common tax base for multinationals - again . June 17, 2015. Retrieved July 7, 2015.

- ↑ European Commission half measures will exacerbate profit shifting . June 17, 2015. Retrieved July 7, 2015.

- ↑ EU's anti-tax avoidance package likely to fail, say NGOs . In: Euractiv.com . January 28, 2016. Accessed March 31, 2016.

- ↑ EU offers new plan to tackle corporate tax dodging . In: reuters.com . April 12, 2016. Retrieved June 3, 2016.

- ↑ EU struggles to close tax loopholes with new law . In: EU Observer . June 22, 2016. Retrieved December 3, 2016.

- ↑ Brussels aims to harmonize corporate tax by 2021 . In: Euractiv.com . October 27, 2016. Retrieved December 3, 2016.

- ↑ European Parliament, TAXE committee

- ↑ Tagesschau, "Luxleaks" affair about tax dumping clarification, yes, but ... ( Memento from February 6, 2015 in the Internet Archive ), February 5, 2015

- ↑ Deutschlandfunk, Luxleaks - The Enlightenment Is Sabotaged , May 6, 2015

- ^ David Pegg: MEPs offer support to convicted LuxLeaks whistleblowers. In: theguardian.com. September 8, 2016, accessed September 14, 2016 .

- ^ Luxembourg accuses. Süddeutsche Zeitung from December 12, 2014.

- ↑ Bastian Obermayer: I wasn't alone. Süddeutsche Zeitung from December 14, 2014.

- ^ STANDARD Verlagsgesellschaft mbH: Whistleblower Deltour: The price of truth . In: derStandard.at . ( derstandard.at [accessed on February 6, 2017]).

- ↑ http://www.lemonde.fr/societe/article/2016/04/26/le-proces-des-luxleaks-s-ouvre-a-luxembourg_4908549_3224.html

- ↑ inculpation d'un journaliste français communiqué par la Parquet de Luxembourg, 23 April 2015

- ↑ sueddeutsche.de April 23, 2015: Luxembourg takes action against Luxembourg leaks journalists

- ↑ NDR, Zapp, Luxleaks: Investigations against the uncoverer , May 19, 2015

- ↑ a b AFP: LuxLeaks prosecutors seek jail term of 18 months for whistleblowers. In: theguardian.com. May 10, 2016, accessed May 12, 2016 .

- ↑ Antoine Deltour - Lux-Leaks-Whistleblower threatens prison sentence , Süddeutsche Zeitung, April 26, 2016

- ↑ Luxleaks process kick-off - access to PwC documents was easy for Deltour , Das Wort, April 26, 2016

- ↑ Arthur Neslen: Luxleaks trial of tax whistleblowers begins in Luxembourg . In: The Guardian . April 26, 2016, ISSN 0261-3077 ( theguardian.com [accessed February 6, 2017]).

- ↑ https://www.change.org/p/soutenons-antoine-deltour-luxleaks-support-antoine

- ↑ Jon Schwarz: Reporter and Whistleblowers On Trial for Ruining Luxembourg's Tax Avoidance Fairyland. Retrieved February 6, 2017 .

- ↑ Luxleaks: Antoine Delta Tour: herói ou vilão em julgamento . In: Wort.lu . April 27, 2016 ( wort.lu [accessed February 6, 2017]).

- ↑ France backs defendant as LuxLeaks trial starts . In: BBC News . April 26, 2016 ( bbc.com [accessed February 6, 2017]).

- ↑ L'essentiel: France wants to help whistleblower Deltour . In: L'essentiel in German . ( lessentiel.lu [accessed February 6, 2017]).

- ↑ https://www.luxprivat.lu/news/detail/liberation-der-komische-luxleaks-richter-marc-thill.html "Liberation": The funny Luxleaks judge Marc Thill. This is how Luxembourg's “independent judiciary” works.

- ↑ http://www.liberation.fr/france/2016/04/27/proces-luxleaks-la-justice-luxembourgeoise-en-question_1449031 Procès LuxLeaks: la justice luxembourgeoise en question

- ↑ Procès LuxLeaks: la justice luxembourgeoise en question… In: Libération.fr . ( liberation.fr [accessed February 6, 2017]).

- ↑ Prison sentences on probation Tageblatt , June 29, 2016, accessed on the same day.

- ↑ Harald Neuber: Suspended sentences and fines in the “Luxleaks” process. Telepolis , June 29, 2016, accessed the same day.

- ↑ Court conceded judgment against Luxleaks-whistleblower Spiegel Online, 11 January 2018

{kind=link}